In Focus – SCCCU Blog

Stay informed about the Credit Union’s activities, plus get practical advice on a variety of personal finance topics.

Allowances 101: Should You Give Your Child an Allowance?

In the age of digital and mobile everything, it should come as no surprise that even something as old-fashioned as a child’s allowance has evolved. Here’s a look at the new rules for giving your child an allowance and what you need to know.

Thankfully, more parents are talking to their kids about money today than ever before. According to the 14th annual Parents, Kids, & Money survey by T. Rowe Price, 49% of parents are talking to their kids about money. While we wish the number was 100%, knowing that half of all families are having financial conversations is great news. Kids need to learn financial skills, and starting at home paves the way to lifelong money literacy.

Besides talking, though, kids need direct practice with money and making decisions. What’s the best tool for that? An allowance, says John Lanza, author of “The Art of Allowance.”

Lanza says that effective money lessons come in three parts: direct instruction, modeling from the parents, and giving kids experiences with money. “Teaching kids about money is an opportunity to share your values around what you think matters, whether that’s frugality, paying yourself first, or charitable giving and how much,” he says. But kids also need to make their own decisions and mistakes. Those will resonate more than a parental lecture — and that’s exactly where an allowance comes in.

When giving an allowance, Beth Kobliner, author of “Make Your Kid a Money Genius (Even if You’re Not),” recommends what she calls the 4 Cs: Be clear about what the money is for, be consistent about giving it, use cash (more on this in a minute), and don’t tie it to chores. She also recommends a fifth C: control, meaning your child should have control over their cash — with a little input from mom and dad. Of course.

Many parents have strong opinions about not giving what they consider to be a “handout,” especially when finances are tight. The most important thing is that you figure out what works for your family at a given time — there’s no “perfect” way to handle an allowance, and if it’s not in the budget, there are tons of ways to teach money lessons for free — more on that below!

The Argument for NOT Tying an Allowance to Regular Chores

An allowance is a tool to learn about money, Lanza says. The goal is to open up positive conversations around the skills you want kids to learn. “When you tie allowance to chores, you’re setting yourself up for using allowance in a punitive way,” he says. What happens if your kid skips her chores? Develops a habit of rushing just to be paid? “There’s a bit of a cloud that starts to hang over the conversation,” he says. The chore focus shifts the conversation away from financial literacy.

That doesn’t mean your kid doesn’t do chores or that they won’t learn the value of work. “Doing unpaid chores around the house encourages your kid to develop internal motivation, which will help them down the line,” Kobliner says. Learning about money and chores are both important, but kids are learning different things from each conversation, and it’s easier to teach those lessons if you keep them separate.

It’s also perfectly fine to pay for optional above-and-beyond chores — things like cleaning the garage, shoveling snow, or raking leaves. Your child gets the experience of working for money and developing an entrepreneurial spirit. That’s a different skill set from pitching in with family chores.

When and How to Start an Allowance

You can start offering your child an allowance younger than you think, possibly by age 4 or 5 or once kids start school. Some experts suggest offering around $20 per month, but you can offer more or less depending on the age of the child, the lessons you hope to teach, what you are expecting your child to pay for with the money (you can give more through the years if you increase the things that they have to pay for with “their money”) and your family’s budget.

Lanza suggests having three jars where your child can keep their money — a “save jar” for money to be saved for the future, a “spend jar” for money that can be spent now, and a “share jar” for charitable contributions. Let’s say you give $5 per week to your 5-year-old. That might divide up into $1/save, $3/spend and $1/share, (20%/60%/20%). The goal is to give kids enough spending money that they have some purchasing power and room for decisions, but they also develop a regular habit of saving and giving.

The added benefit of the jars? It takes you out of the driver’s seat when you’re in the grocery store line being hit with requests for comic books and candy. Once you’ve established rules for the categories that you aren’t going to be covering, let your kids decide what they want most — it’s their allowance. And many times, they’ll be much more responsible with their own money than they will be yours, Lanza says.

Also, your kids will learn more about money when you kick it old-school and give them cash. They learn better via hands-on experience, with real bills and coins to put into their jars. Kobliner recommends offering your child a cash allowance through high school. Just make sure you transition to debit cards and apps before kids leave home for college so they can practice with digital payment methods, Lanza says. (Why is cash so important? Research shows that parting with cash makes us think more critically about our purchases than if we’re just swiping a credit card — and kids need to learn to manage the card temptation.)

Increase Financial Responsibility with Age — If You Have It in Your Budget

When kids are very little, they’ll use their small allowance for incidental spending, and you likely won’t be giving them very much. But once kids hit middle school, Lanza recommends what he calls a “break-through allowance.” That’s a larger allowance given monthly that may come with increased responsibility, such as paying their portion of their cell phone bill, putting money toward meals out with friends, or buying new clothing. Every family operates differently, so you get to decide what’s right for yours.

If a larger allowance sounds beyond your means, remember that the goal here isn’t to add a large line item to your budget — it’s to shift some of your own spending over to your child. (Like buying gas for their car, for example.) Start by tracking the spending you’d like to turn over to your child to identify an appropriate amount. The goal is that they’ll learn to make important choices about their spending — don’t bail them out if they spend all their money early in the month or buy something they regret.

Why Allowances Work

The true benefit of giving your kid an allowance is the conversations it opens up for your family to discuss the value of money, how to pay for goods, and the difference between needs and wants. Exposing your kids to financial literacy early is the best way to make them comfortable with money… And help you get more comfortable, too! Even if you’re not the best with money, you’ll have an opportunity to learn as you go with your kids, and as you do, your own comfort will grow.

- CATEGORIES: Financial Education

Protect Yourself from “Vacation Recovery” Scams

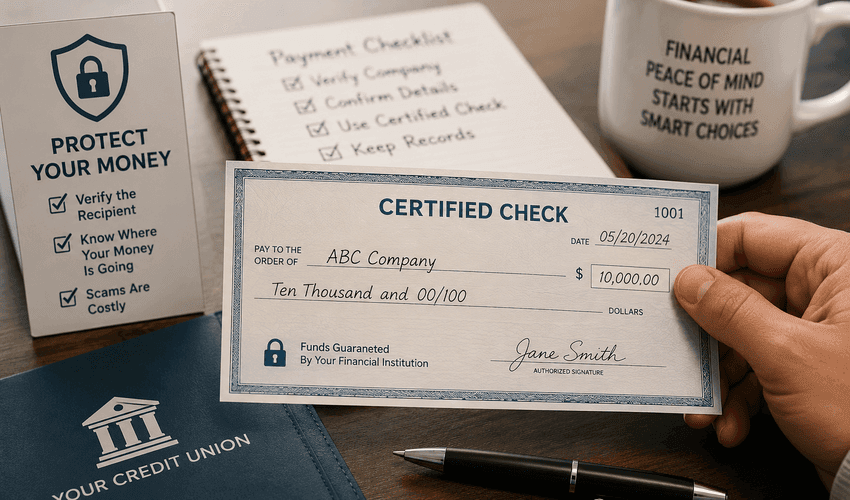

A Certified Check Doesn’t Protect You From a Scam